")

Originally posted, 19 Jan 2024 – Battery Metals in 2024 – Five Key Themes to Watch

In 2023, battery raw materials dominated headlines with stories of softening prices, the question of fragmentizing supply chains in light of the China-U.S. rivalry and the continuous build-up of capacity to support the electrification of the global passenger car fleet. Investment in infrastructure was in no small part due to government activity, with firms trying to capture subsidies offered by the Inflation Reduction Act (“IRA”) in the U.S. and similar programs elsewhere. While prices softened in light of an oversupplied market, the long- term trends remain intact and point towards higher electric vehicles (EV) penetration rates and stronger demand for the metals required to produce those cars.Here are five battery metals themes to watch out for in in 2024.

Cobalt prices: lower for longer or rebound?

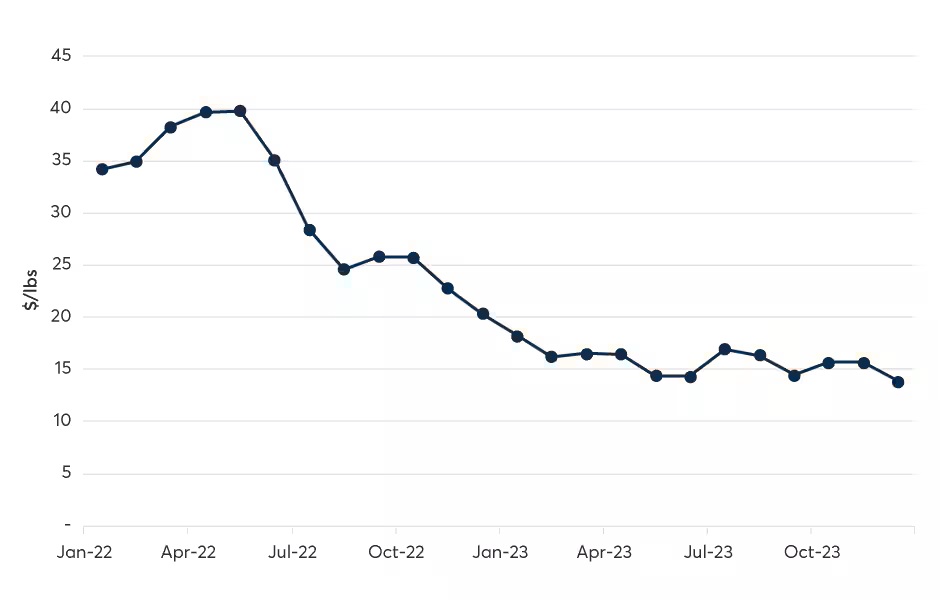

Since hitting multi-year highs of around 40 $/lb. in mid-2022, cobalt spot prices have been trending downward, and spent the majority of the year somewhere between 13 and 20 $/lb. Market supply is solid with CMOC Group Limited (CMOC), a Chinese company active in the Democratic Republic of the Congo (DRC), announcing that its 2023 output increased 174% YoY to over 55,000 metric tons, thereby becoming the world’s largest producer[1] ahead of Swiss-based Glencore. At the same time, Indonesian production continues to grow, with volumes increasing fivefold in two years[2]. On the demand side, cobalt bulls may find solace in the fact that global air travel is rebounding, boosting the order books of Airbus and Boeing – which could mean higher demand for cobalt as a high-resistance alloy in the aerospace industry. In the battery sector, no-cobalt batteries, especially the LFP (lithium-iron-phosphate) kind, are expected to progressively increase their share of the total. This will lower the average cobalt intensity of batteries, but higher total demand for EVs (discussed in detail below) should more than offset this effect.

For 2024, market participants will watch closely if continuous low prices will force some high-cost producers out of the market.

Cobalt Metal spot month prices

Source: CME Group – Past performance is not indicative of future results

China and lithium markets

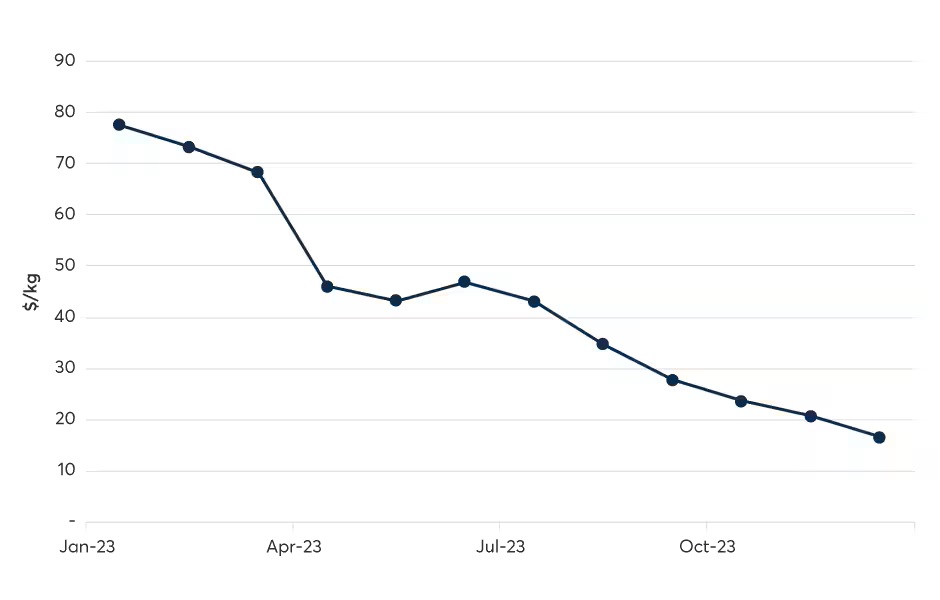

Misery loves company so it is maybe fitting that lithium prices followed cobalt’s downward path in 2023. The market for lithium hydroxide started the year at all-time highs of around $80 /kg but finished at below $20/kg. Market analysts have pointed to a well-supplied market, with African production surprising on the upside and muted demand, notably a destocking occurring in the Chinese EV manufacturing sector. At the same time, this slowdown hasn’t stopped Chinese firms defending their leading position in the global EV market, with Chinese car manufacturer BYD delivering 526,000 EVs in the fourth quarter 2023 alone, and thereby overtaking Tesla for the first time[3]. If low prices continue for longer, market watchers think it is mainly the non-integrated refiners (those that buy spodumene and produce chemicals) that are in loss-making territory[4] and therefore at risk.

In 2024 and beyond, participants will pay attention to whether the mining sector is able to continue to deliver new production capacity. Greenfield mining projects are often at risk of multi-year delays, and lithium is no exception.

Lithium Hydroxide spot month prices

Past performance is not indicative of future results

U.S. Elections and the IRA

The Inflation Reduction Act is seeking to create an U.S. centric supply chain for electric vehicles. Tax credits for consumers and manufacturers is intended to create solid domestic demand for electric vehicles and incentivize local production as well as processing of the raw materials and batteries needed. More than $70bn of investments in the U.S. battery supply chain have been announced since the IRA came into force[5]. Could a new administration following the presidential election in November put the IRA at risk? This is no foregone conclusion, since a majority of the IRA funded projects announced to date are located in ‘red states’[6], meaning that local politicians could oppose a radical overhaul of those policies that attracted investment and created jobs in their districts in the first place.

Efforts to create a less China-centric supply chain is not restricted to the U.S. The EU Critical Raw Materials Act aims to achieve something similar, meaning that we may see bifurcated supply chains emerging in 2024, with some commodities or intermediate products eligible for use in one region but not the other.

EV sales trends

Press coverage over the past months could lead observers to believe that the EV sector is hitting significant roadblocks – Ford announced it is postponing a $12bn EV investment plan, GM abandoning EV production targets of 400,000 units built by mid-2024, and Volkswagen cancelling plans for a new EV factory[7]. Yet, at the same time, EV penetration rates of new vehicles sold are at record levels, with BloombergNEF forecasting 14.2m passenger electric vehicles sold in 2023, versus 10.5m the year prior[8], and even higher numbers forecast for 2024[9]. Possibly, EV manufacturers have had to correct overly optimistic assumptions, as the EV market is now also targeting mass market clients rather than luxury buyers and early adopters. The decrease in commodity costs, which are the main component of the battery cost stack – itself the highest value item in an EV – will be welcomed by those manufacturers.

‘Electric vehicles’ do not only mean passenger cars– a significant portion of EV sales growth out of Asia will be two- and three-wheelers. For instance, from January to October 2023, sales of electric two-wheelers in India increased 50% versus the same period one year prior[10]. Driven by subsidies and an expanding infrastructure to swap batteries on-the-go, this trend is expected to continue. The EV adoption in the commercial vehicles sector is also accelerating.

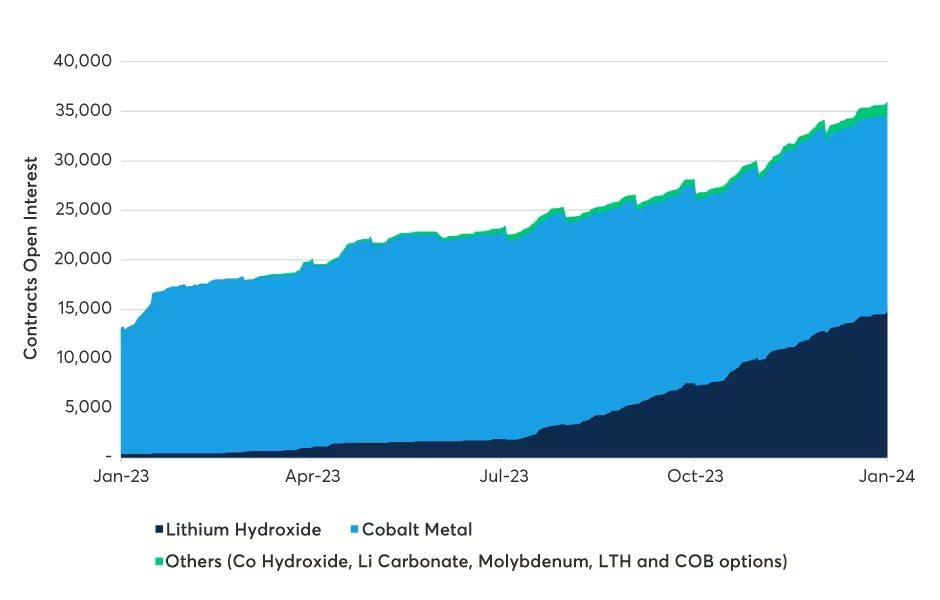

Continued growth in derivatives markets: growing liquidity and more products

Mirroring the growth in physical volumes being mined and processed, trading in cobalt and lithium derivatives has continued to grow throughout 2023. In light of a volatile price environment, market participants have relied on battery metal futures listed on CME Group. Higher liquidity in the contracts has also led to demand for new products, and to address this interest, the Exchange added, in 2023 alone, a cobalt hydroxide futures contract, lithium carbonate futures, as well as options on the existing lithium hydroxide and cobalt metal futures. While most of the trading is still in the well-established cobalt and lithium contracts, these additional products should allow market participants even more granular hedging of risk and trading opportunities.

Open interest in battery contracts on CME Group

Source: CME Group – Past performance is not indicative of future results

References

[1] https://www.bloomberg.com/news/articles/2024-01-04/chinese-miner-takes-glencore-s-cobalt-crown-as-output-jumps-170

[2] https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/metals/080323-indonesia-emerging-as-major-cobalt-supplier-amid-lingering-esg-concerns

[3] https://www.reuters.com/business/autos-transportation/teslas-fourth-quarter-deliveries-beat-estimates-2024-01-02/

[4] https://www.gspublishing.com/content/research/en/reports/2023/11/30/781bb7c9-e771-4413-a6f3-e3ae9bd33327.html

[5] https://www.energypolicy.columbia.edu/wp-content/uploads/2023/09/US-IRA-Commentary_CGEP_103023.pdf

[6] https://www.ft.com/content/06fcd3dd-9c39-48d3-bb08-6d75d34b5ed1

[7] https://www.forbes.com/sites/michaelharley/2023/10/30/5-reasons-why-electric-vehicle-sales-have-slowed/?sh=16619c0f5110

[8] https://assets.bbhub.io/professional/sites/24/2023-COP28-ZEV-Factbook.pdf

[9] https://www.spglobal.com/mobility/en/research-analysis/2024-ev-forecast-the-supply-chain-charging-network-and-battery.html

[10] https://auto.economictimes.indiatimes.com/news/industry/ev-penetration-to-grow-exponentially-sectors-profitability-expected-to-delay-take-off/105009256

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.