")

Originally posted, 04 January 2024 – As Inflation Retreats, How Will Equities Perform in 2024?

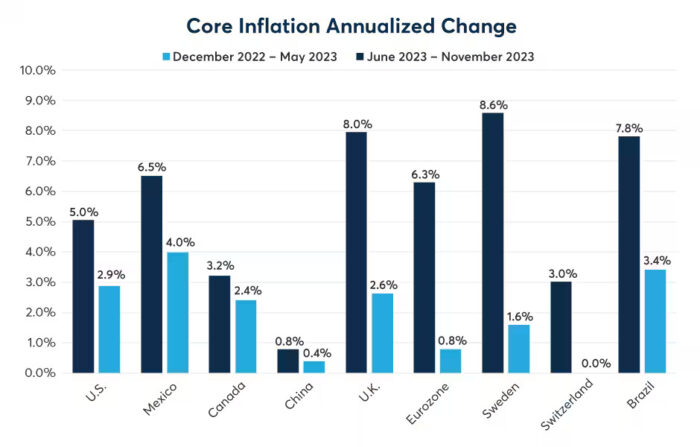

During the 1990s and again in the 2010s, equity and bond investors celebrated a goldilocks economy. GDP and employment growth were solid and core inflation remained comfortably around 2% per year despite increasingly tight labor markets. That scenario was occasionally interrupted, notably by the tech wreck recession in 2001, the 2008 global financial crisis, and most recently by the pandemic-era surge in inflation. But by late 2023, inflation appeared to be coming down globally. Comparing the annualized inflation rates during the six months from December 2022 to May 2023, and the six months from June to November 2023, inflation rates have fallen sharply in every major economy (Figure 1).

Figure 1: Core inflation rates are falling rapidly worldwide

Past performance is not indicative of future results

Granted, things still don’t feel great for consumers, who appear to be less sensitive to the rate of change in prices than they are to level of prices which remain high and are still climbing, albeit at a slower pace than before.

Nevertheless, it appears that the main drivers of inflation — supply chain disruptions (Figure 2) and surging government spending (Figure 3) — subsided long ago. Supply chain disruptions sent the prices of manufactured goods soaring beginning in late 2020. Depressed pandemic-era services prices initially masked the surge in inflation, but services prices began soaring as the world reopened in 2021 and 2022 driven by surging government spending, which created new demand but no new supply of goods and services. Since then, however, supply chain disruptions have faded despite Russia’s invasion of Ukraine, and with little impact thus far from the conflict between Israel and Hamas. Moreover, government spending has rapidly contracted as pandemic-era support programs have expired despite some increases in spending related to infrastructure and the military. As such, not even the low levels of unemployment prevailing in Europe, U.S. and elsewhere appear to be sustaining the rates of inflation witnessed in 2021 and 2022.

Figure 2: Supply chain disruptions drove inflation in manufactured goods in 2020 and 2021.

Past performance is not indicative of future results

Figure 3: U.S. government spending has fallen from 35% to 22.6% of GDP

Past performance is not indicative of future results

U.S. core CPI is still running at 4% year on year but its annualized pace slowed to 2.9%. What’s more is that in the U.S. most of the increase in CPI has come from one component: owners’ equivalent rent, which imputes a rent that homeowners theoretically pay themselves based off actual rents on nearby properties. Outside of owners’ equivalent rent, inflation in the U.S. is back to 2%, its pre-pandemic norm (Figure 4).

Figure 4:U.S. inflation is much lower when excluding home rental

Past performance is not indicative of future results

Moreover, inflation in China has been running close to zero in recent months and has sometimes even shown year-on-year declines. In China, real estate grew to be as much as 28% of GDP, and the sector is now rapidly contracting. China’s year-on-year pace of growth for 2023 looks solid at around 5%, but that’s not too impressive given than the year-on-year growth rate compares to 2022, when the country spent much of the year in COVID lockdowns. By the end of 2023, China’s manufacturing and services sectors were both in a mild contraction, according to the country’s purchasing manager index data. If growth doesn’t improve in 2024, China may export deflationary pressures to the rest of the world.

That doesn’t mean that the are no upward risks to prices. If the Israel-Hamas war broadens and interrupts oil supplies through the Suez Canal, that could reignite inflation. Moreover, green infrastructure spending, rising military spending, near-shoring as well as demographic trends in places like South Korea, Japan, China and Europe that limit the number of new entrants in the global labor market could potentially keep upward pressure on inflation. For the moment, however, any inflationary impacts from geopolitical or demographic factors appear to be overwhelmed by the usual set of factors keeping inflation contained including technological advancement and large labor cost differentials among nations.

So, what does this mean for investors? As we begin 2024, fixed income investors are pricing about 200 basis points (bps) of rate cuts by the Federal Reserve over the next 24 months, and the S&P 500 is trading close to a record high. Be warned, however, interest rate expectations have been extremely volatile over the past 12 months, oscillating between expecting rate hikes to rate cuts by as many as 200 bps or more (Figure 5). If we continue to see strong employment and consumer spending numbers combined with weakening inflation numbers, this may keep rate expectations caught in a volatile crosscurrent.

Figure 5: Investors price steep Fed cuts but rate expectations are extremely volatile

Past performance is not indicative of future results

Moreover, while equities did well in 2023, their rally was narrow, driven by only a handful of large tech and consumer discretionary stocks, while most other stocks including small caps were largely left behind. Finally, the stock market itself isn’t cheap. The S&P 500 is trading at 23.37x earnings and the Nasdaq 100 at 59x earnings. As a percentage of GDP, the S&P 500’s market is still close to historic highs. Finally, even with 2023’s rally, the indexes are trading at basically the same levels at which they ended 2021 (Figure 6). Part of the reason stocks did so well in the 1990s and 2010s is that they started out those decades cheap. The same cannot be said of the starting values for 2024 (Figure 7).

Figure 6: Nasdaq and S&P 500 are near end of 2021 levels but the Russell 2000 lags behind

Past performance is not indicative of future results

Figure 7: Going into 2024, equities aren’t cheap like they were in 1994 or 2014

Past performance is not indicative of future results

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.