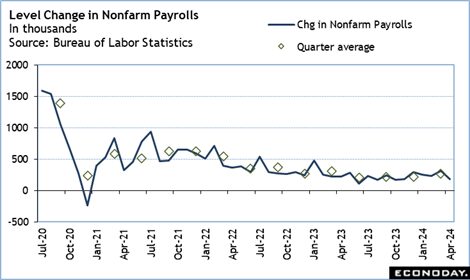

The May 6 week presents a remarkably empty calendar for US economic data. This will leave plenty of time to speculate about the direction of Fed monetary policy after the downside surprise in the change in nonfarm payrolls with April coming in with a 175,000 increase and a net downward revision of 22,000 to the prior two months. This compares to the consensus estimate of 243,000 in April in the Econoday survey of forecasters. The unemployment rate came in as expected at 3.9 percent.

To be sure, this is only a softer-than-expected reading on payrolls for one month and is by no means a weak report in the historical context. However, markets have been disappointed by the recent hawkish tone of comments by Fed policymakers based on the current economic data. The consequent lengthening anticipation of a rate cut has tightened conditions in financial markets. Those sectors most sensitive to interest rates may find cause for optimism that the prospects of a rate cut a bit sooner have improved. It is far too early to speculate that the outlook for interest rate policy has changed.

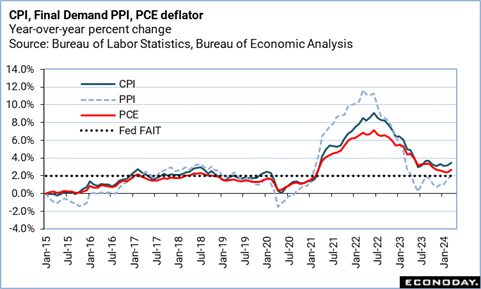

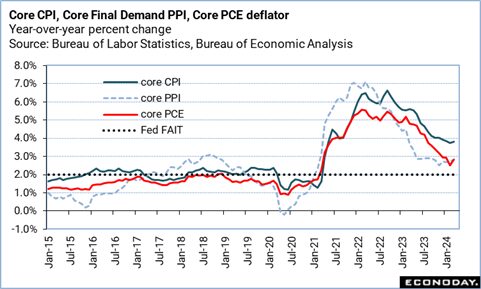

If nothing else, Fed Chair Jerome Powell has cautioned that the FOMC is not going to overreact to one month’s worth of data and will need more than one data point to change its thinking. This was said in reference to the stall in the inflation indicators’ progress but can be equally applied to the labor market.

At his press briefing on May 1, Powell signaled that the fed funds target rate is thought to be at its cyclical peak at 5.25-5.50 percent. Further tightening is unlikely, although possible if deemed appropriate by the FOMC. Much more likely is a reduction in rates, but only when the economic data offer “greater confidence” that inflation has been thoroughly tamed and/or maximum employment needs a nudge with some monetary stimulus. Right now, the balance of risks for either half of the dual mandate are about even. As long as the economy exhibits tempered expansion with a healthy labor market and disinflation is not as advanced as the FOMC would like, the Fed will be on hold.

Markets should defer any change in their expectations until after the May employment report on Friday, June 7. This will be only days before the June 11-12 policy meeting at which the FOMC will update the quarterly summary of economic projections (SEP). Even if the April inflation reports show a resumption of the disinflationary trend, it will still be only one months’ worth of numbers. The April CPI report is set for 8:30 ET on Wednesday, May 15 and the PCE deflator for April at 8:30 ET on Friday, May 31.

Past performance is not indicative of future results

—

High points for US economic data scheduled for May 6 week

Disclosure: Econoday Inc.

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.