")

Originally Posted, 26 Feb 2024 – What’s Hot: Tin gains momentum in lockstep with the technology cycle

Key Takeaways

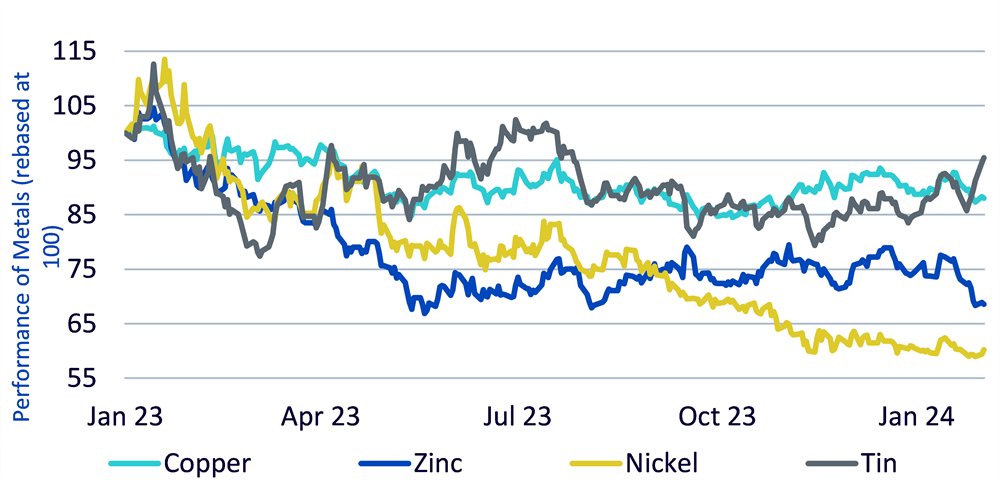

- Tin has been outperforming the industrial metals complex over the past year on the back of improving fundamentals

- Demand for Tin is benefitting from an upswing in the global technology cycle

- Tin’s supply chain remains under political threat

- Related Products WisdomTree Tin Find out more

Tin has been outperforming the industrial metals complex over the past year on the back of improving fundamentals. The improvement in fundamentals has been supported by weak supply, with mine production hardly moving above 300 kilotonnes (kt) over the past 20 years. At the same time, demand has gained support by an upswing in the global technology cycle. Tin is instrumental in manufacturing semiconductors, solar panels, 5G technologies and electric vehicles – a wide suite of demand sources. As the market for tin is relatively small at around 300kt compared with other industrial metals (i.e. copper at 25Mt), it is often overlooked by investors. A closer look at tin is warranted as demand for tin strengthens from growing adoption of technologies alongside the supply chain remaining under political threat.

Figure 1: Comparison of Tin’s performance versus industrial metals over the past year

Source: Bloomberg, WisdomTree as of 13 February 2024. Historical performance is not an indication of future performance and any investments may go down in value.

Long term demand for tin should benefit from improving global technology cycle

Tin stands out among industrial metals owing to its heavy exposure on the demand side to the green energy transition and technology sector. So, while industrial metals performance has been dampened by property sector woes and the weaker growth backdrop in China, tin’s performance has been aided by higher demand from the improving global technology cycle. An important source of demand is the use of tin for solder – joining circuit boards in semiconductors in addition to solder ribbon to join solar panels. This puts tin in a unique spot compared to industrial metals as its utility in the property sector is far outweighed by its role as a conductive metal in technologies such as EVs, renewable energy and consumer electronics. In fact, tin ore imports from China rose 2.1%YoY in 2023 . More importantly, imports into China have been rising consistently on an annual basis since 2019, despite macro headwinds facing its economy.

Tin supply has been challenged

The main tin-producing countries are China, Indonesia, Myanmar and Peru1. Total reserves, which include current and prospective operations, represent 16 years of extraction, with the biggest deposits prevalent in China (23%), Indonesia (16%), Burma (14%), Australia (12%), Brazil (9%) and Bolivia (8%)2.

China, currently the world’s largest producer and consumer, has struggled to significantly increase supplies from its own mines despite higher domestic demand. To fill the gap, Myanmar was able to increase its market share, making it China’s top supplier. Yet shipments from Myanmar were disrupted in 2023, as the government in Wa State, a key mining region in Myanmar, imposed a mining ban in August 2023. This resulted in a significant decline in exports to China at the end of last year. With inventories falling of late and Myanmar’s mine production falling by more than 5kt in Q4 2023, Chinese smelters will need to find alternative sources of supply3. The government in Myanmar raised export taxes on tin concentrates from 7th February.

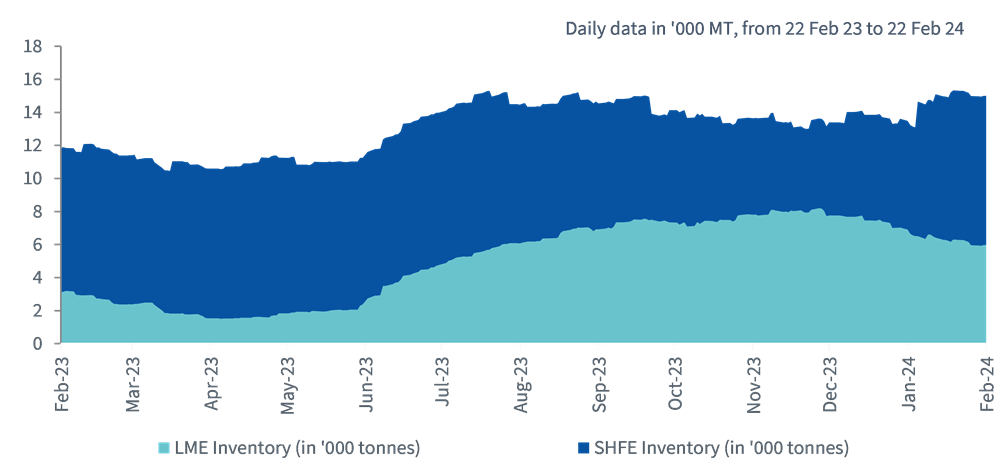

Indonesia, the world’s second largest producer of refined tin has seen output contract materially over the years with supply falling to half of what it did in the past. Reflecting this trend, exports underperformed last year, dropping by 12% YoY2. LME inventories of tin have continued to decline, largely owing to exports from Indonesia dropping to just 0.4t in January over changes in the mine permitting processes.

While stocks in LME warehouses rebounded to above 8kt towards the end of 2023, they are still significantly below historical peaks. The global tin market is likely to remain in a deficit in Q1 2024 (seasonally production tends to fall while demand remains steady). However, as exchange stocks are higher this year, it could allow supply to outpace demand. Over the long run, the supply chain remains under political threat at a time when demand is benefitting from an improvement in the global technology cycle, which should continue to support tin prices higher.

Figure 2: Tin inventories

Source: Bloomberg, WisdomTree as of 13 February 2024. Historical performance is not an indication of future performance and any investments may go down in value.

Investor sentiment towards tin continues to improve

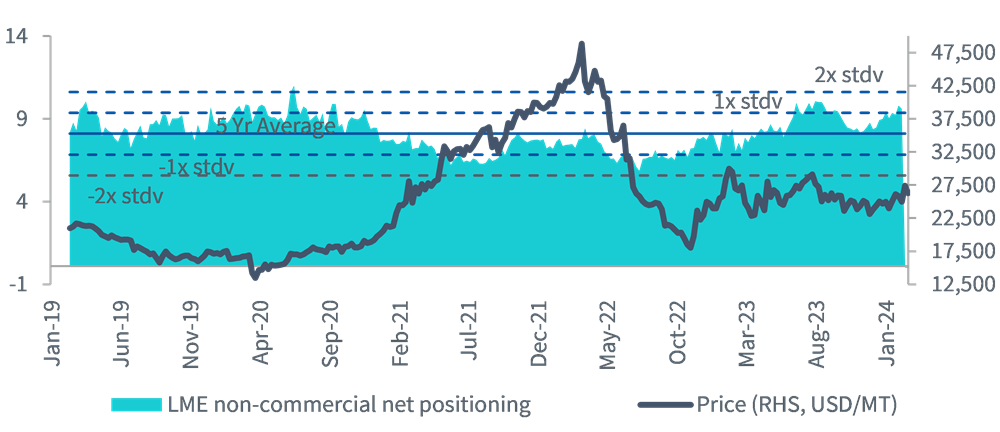

Net speculative positioning in tin futures has been gaining momentum since June 2022. Since May 2023, net speculative positioning has remained above the 5-year average underscoring an improvement in sentiment towards tin.

Figure 3: Net speculative positioning in Tin Futures

Source: Commodity Futures Speculative Commission, WisdomTree as of 6 February 2024. Please note: stdv represents standard deviation. Historical performance is not an indication of future performance and any investments may go down in value.

Sources

1 International Tin Association (ITA) as of 31 July 2023

2 Bloomberg as of 31 December 2023

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.