")

Originally posted 18 March 2024 – Carbon Market News Roundup

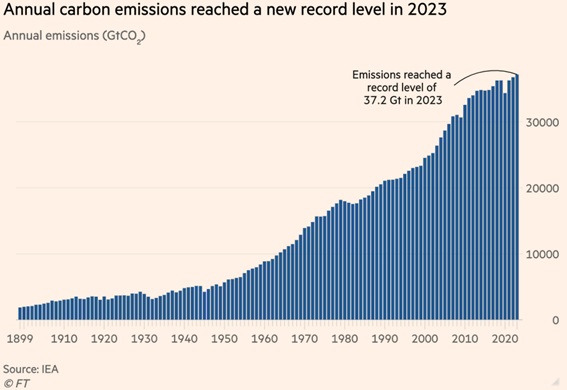

Emissions Rose in 2023…

Global carbon dioxide emissions rose in 2023 according to a recent International Energy Agency (IEA) report. 37.4 billion metric tonnes of CO2 were emitted, a 410-million-tonn-increase compared to 2022 (about a 1.1% increase). The rise is attributed to the increase in fossil fuel use due to droughts (exacerbated by El Niño and climate change, which then in turn resulted in a record decrease in hydropower output) and rising energy demand across the developing world, with the contributions of China and India more than offsetting the falling use of fossil fuels in advanced economies like the EU and US.

Emissions from fossil fuel use in China grew by 5.2%, with a 6.1% increase in energy demand from sectors like construction. In contrast, use of fossil fuels in energy production in the US dropped 4.1% despite the economy growing 2.5%, influenced by lower gas prices driving out coal. In the EU, emissions from energy fell nearly 9% despite economic growth of 0.7%, with electricity production from coal and gas being overtaken by wind power for the first time.

Despite Higher Investment in Renewables.

Given the geopolitical, economic, and climate-related factors influencing energy production and demand over 2023, perhaps it isn’t surprising that emissions grew, especially in developing countries. However, record greenhouse gas emissions last year coincided with record global investment in clean energy. For the Chinese case, the country accounted for around 60% of new solar and wind energy, as well as electric vehicles (EVs) developed during 2023.

In fact, global investment in the green energy transition reached nearly $1.8 trillion in 2023, an all-time high and an impressive 17% increase over 2022.

Electrified transport (which includes spending on EVs and infrastructure for charging) overtook renewables and became the most-invested sector at $634 billion. While nuclear, electrified heat, and clean shipping all saw a slight decline from 2022, all other sectors performed well: hydrogen tripled, carbon capture and storage (CCS) almost doubled, energy storage grew 76%, and clean industry grew 7%. Power grids (necessary for the electrification of modern life) saw $310 billion spent in 2023.

As mentioned above, China leads the pack in investment.

The energy transition saw $676 billion invested in China alone last year, representing nearly 40% of the global investment. The US was second at $303 billion, with the effects of the Inflation Reduction Act’s energy transition incentives beginning to kick in. However, if counting the European Union as a whole, the bloc outspent the US at $341 billion (over $400 billion if the UK is included). A significant development is that the US + EU + UK level of investment exceeded that of China’s, which was not the case in 2022.

Looking at the chart below, it’s clear that the private sector is increasingly interested addressing emissions as well:

Source: Nat Bullard

But Is It Enough for Net-Zero?

Is the incredible amount of money being spent on the energy transition enough to see a world with net-zero emissions by 2050? The IEA forecasts that energy-related emissions are in a “structural slowdown” due to the development of clean energy, and estimates that the growth of emissions over the last half-decade would have been tripled if not for the development of clean energy technologies. The agency also hailed the resilience of the global energy transition in the face of the Covid-19 pandemic, an energy crisis, and fraught geopolitical tensions.

At the same time, the agency called for even greater action, especially in emerging economies that still rely heavily on traditional energy sources.

According to BloombergNEF’s net-zero scenario, there is still a $3 trillion investment gap over the rest of the decade to reach net-zero. Investments in electrified transport, renewables, power grids, and energy storage must double, while hydrogen, nuclear, and CCS investments must grow even more. It will take coordination from all sectors, public and private, as well as international organizations and global leaders to bridge this tremendous gap.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Fundamental Analytics and is being posted with its permission. The views expressed in this material are solely those of the author and/or Fundamental Analytics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.